Summary of Local Government Pension Scheme (LGPS)

LGPS at a glance

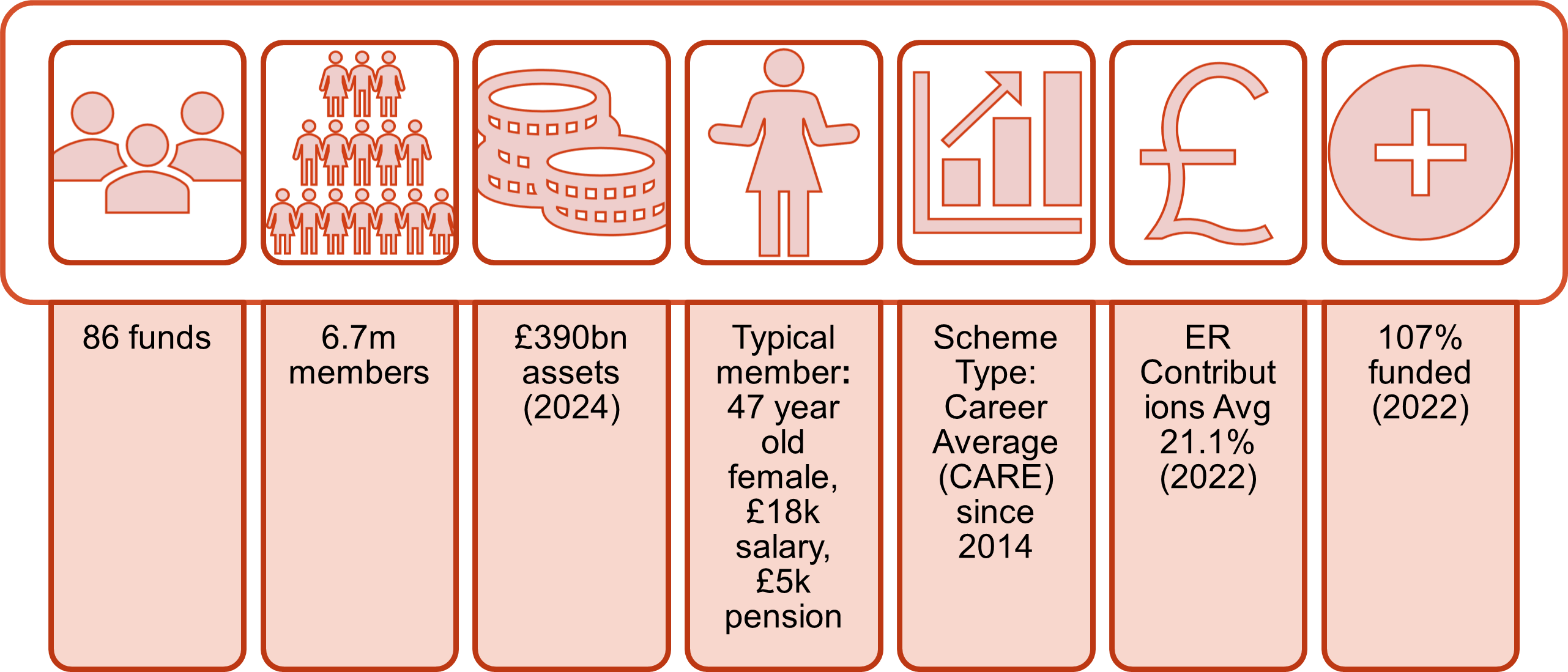

The LGPS in England and Wales is managed by 86 separate scheme managers, each administered by a designated council known as the Administering Authority (AA). The scheme has around 6.7 million members, and as of 31 March 2024 it held £390 billion in assets under management (AUM). More detailed information about the scheme is available in the Scheme Advisory Board (SAB) Scheme Annual Report.

Employees of local government service have a statutory right to join the LGPS under regulation 3 and must be automatically enrolled.

In 2014, the LGPS, ahead of major public sector pension schemes, was reformed from a final salary arrangement to a career average (CARE) scheme following the Hutton Review. These reforms were designed to ensure long-term sustainability. Decisions about the level of benefits provided through public sector pension schemes are set by central government, led by HM Treasury.

Employer contribution rates in the LGPS are determined locally through triennial fund valuations, all of which are published once completed. In 2022, the scheme’s aggregate funding level was 107%, and average total employer contribution rates had fallen to 21.1%, lower than those in other public sector schemes [1]. The next valuation is for the 2025 valuation period, and funding levels are expected to remain above 100%, with contribution rates projected to fall to materially lower levels, likely in the mid‑teens, though final rates will depend on the 2025 valuation results.

The LGPS delivers significant value. A typical member, a 47-year-old woman earning around £18,000 a year, receives an average pension of approximately £5,000 a year. The scheme is also highly efficient: it costs around half as much as the unfunded public sector defined benefit (DB) schemes[2] and helps many members stay above the threshold for means tested benefits. Compared with defined contribution (DC) schemes, the LGPS delivers each £1 of retirement income around 50% more cheaply. Proposals to move new local government employees into DC schemes would likely reduce retirement security, particularly for lower paid workers.

Work of the LGPS Scheme Advisory Board

The Local Government Pension Scheme Advisory Board (SAB) is a statutory body responsible for two key functions: advising the Secretary of State on potential changes to the scheme, and providing guidance to administering authorities and local pension boards.

The SAB has delivered a significant body of work in support of these duties, including:

LGPS Code of Transparency

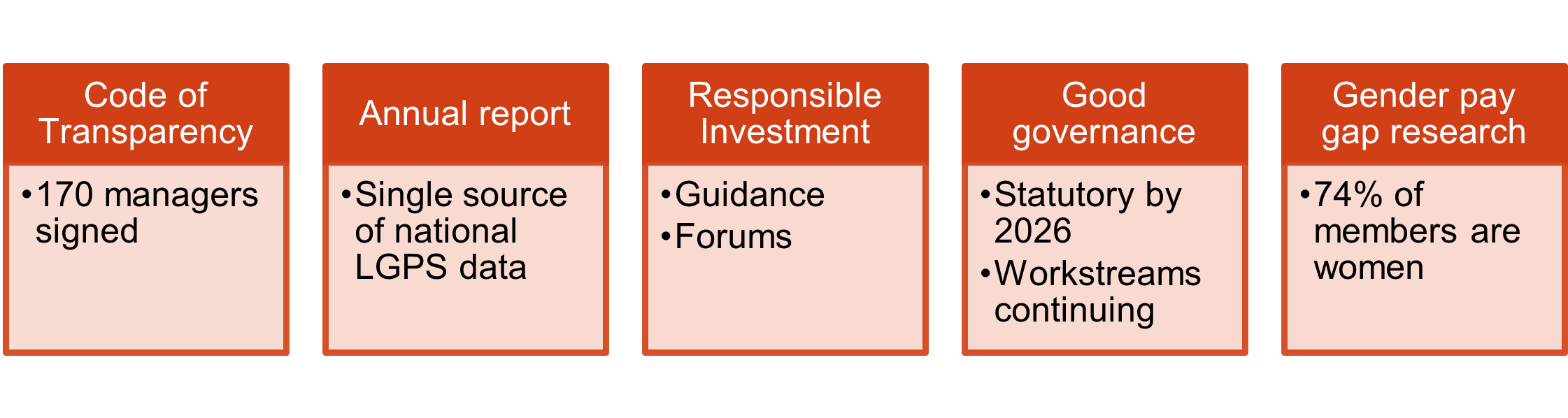

Launched in May 2017, the Code of Transparency was developed by the SAB to improve investment fee reporting and enhance accountability. Around 170 investment managers have now signed up, reflecting strong industry engagement.

LGPS Annual Report

In May 2025, the SAB published its twelfth Annual Report. The report brings together comprehensive information on the status, performance, and governance of the LGPS in a single, accessible source for members, employers, and stakeholders. Continuously improving the quality and consistency of scheme-wide data is one of the SAB’s core priorities.

Responsible Investment (RI) Project

The SAB initiated a major Responsible Investment project in 2019 with the aim of strengthening understanding, governance, and transparency around RI across the LGPS. The project has focused on developing guidance on the governance and regulatory framework underpinning RI decision-making, establishing a Responsible Investment Advisory Group (RIAG) support the Investment Committee (previously named the Investment, Governance and Engagement (IGE) Committee) and the Board, and delivering workshops and seminars for LGPS stakeholders.

Good Governance Project

The SAB’s Good Governance Review produced a series of recommendations aimed at improving standards, clarity, and accountability across the scheme. These recommendations have been accepted by the Ministry of Housing, Communities and Local Government (MHCLG) and are scheduled to become statutory from April 2026.

Gender Pension Gap Project

Research commissioned by the SAB highlights a clear gender pension gap within the LGPS. Women account for 74% of active members, with a mean actual salary of £18,807 and a mean total pension of £3,198. Male members represent 26% of the active membership, with a higher mean salary of £27,532 and a mean total pension of £5,416. This work provides important evidence for ongoing policy development and equality initiatives.

Statutory and fiduciary duties for LGPS administering authorities and asset pool companies

Governance and Decision‑Making

Administering authorities have statutory and fiduciary duties around the investment of pension funds. There are existing statutory controls, the LGPS Investment Regulations 2016, (expected to be replaced by new regulations from April 2026) which ensure that; LGPS funds hold diversified portfolios, explain their approach to non-financial considerations and take professional advice in relation to their investment decisions.

The administering authority normally delegates responsibility for managing the investments of the fund to a pensions or investment committee, where councillors take collective decisions on matters like setting their investment strategy, strategic asset allocations and their responsible investment policy.

Forthcoming Pension Schemes Act (expected April 2026)

The Bill introduces significant new powers, enabling the government to:

- Direct scheme managers into specific LGPS asset pools

- Consolidate pooling into six asset pool companies

- Transfer full asset management responsibility to those pools

Forthcoming secondary regulations will set required content for investment strategies, including:

- Local investment criteria

- Responsible Investment (RI) approaches

Local Investment Framework

The new statutory framework:

- Defines “local investment”

- Requires authorities to set a high-level target range for such investments

- Mandates cooperation with strategic authorities

Although no minimum allocation is required, funds must take account of local economic priorities. Despite the increased emphasis on local investment, the LGPS has historically invested heavily in the UK, 17% of assets were UK based in the 2024 Annual Report.

Responsible Investment Responsibilities

The Act will require investment strategies to clearly set out authorities’ RI priorities and preferences. SAB commissioned legal advice reconfirms that balancing financial and nonfinancial considerations is a core fiduciary function of administering authorities.

Outlook for the LGPS

Recent commentary suggesting that the LGPS should be transformed into a sovereign wealth fund misunderstands both its legal purpose and its existing investment performance. Unlike sovereign wealth funds, which deploy state surpluses for national strategic aims, the LGPS exists solely to fund pensions for nearly 7 million workers. Legal advice and SAB guidance confirm that administering authorities must prioritise members’ retirement outcomes over broader political objectives.

The LGPS remains in a strong and sustainable position, supported by robust funding levels, efficient scheme design and ongoing reforms to ensure it remains fit for the future. Structural improvements, alongside rising funding levels, stable or falling employer contributions and growing investment in UK infrastructure, demonstrate that the scheme continues to evolve responsibly and deliver long-term value for members and employers.

Nationally, wider work under the pensions commission is under way to consider long-term pension adequacy across the whole system, including private sector provision. While the challenges prompting this review are not generally seen within the LGPS, the scheme will continue to contribute constructively to the broader pensions landscape by maintaining strong standards of governance, transparency and long-term planning.

[1] The unfunded public sector DB schemes rates vary from 23.7% (NHS), 28.6% (Teachers), 36.2% (Fire), and 38.7% (Police)

Was this page helpful?