Life Expectancy Index

Introduction

Hymans Robertson and Club Vita have developed an LGPS Life Expectancy Index to support the work of the LGPS Scheme Advisory Board. This index will help support the communication of changing life expectancy in the LGPS to LGPS scheme members. The LGPS Life Expectancy Index will also provide the Board with longevity related information, including early warning of upwards cost pressures to support its role in the cost management process. We have relied upon data provided by Hymans Robertson and its longevity comparison club, Club Vita, when preparing the LGPS Life Expectancy Index.

The information on this page is not specific to the circumstances of any particular reader or organisation, does not constitute advice, nor should it be relied upon by third parties. Life Expectancy Indices may also be produced by other organisations and use other sources of data.

Changes in observed longevity

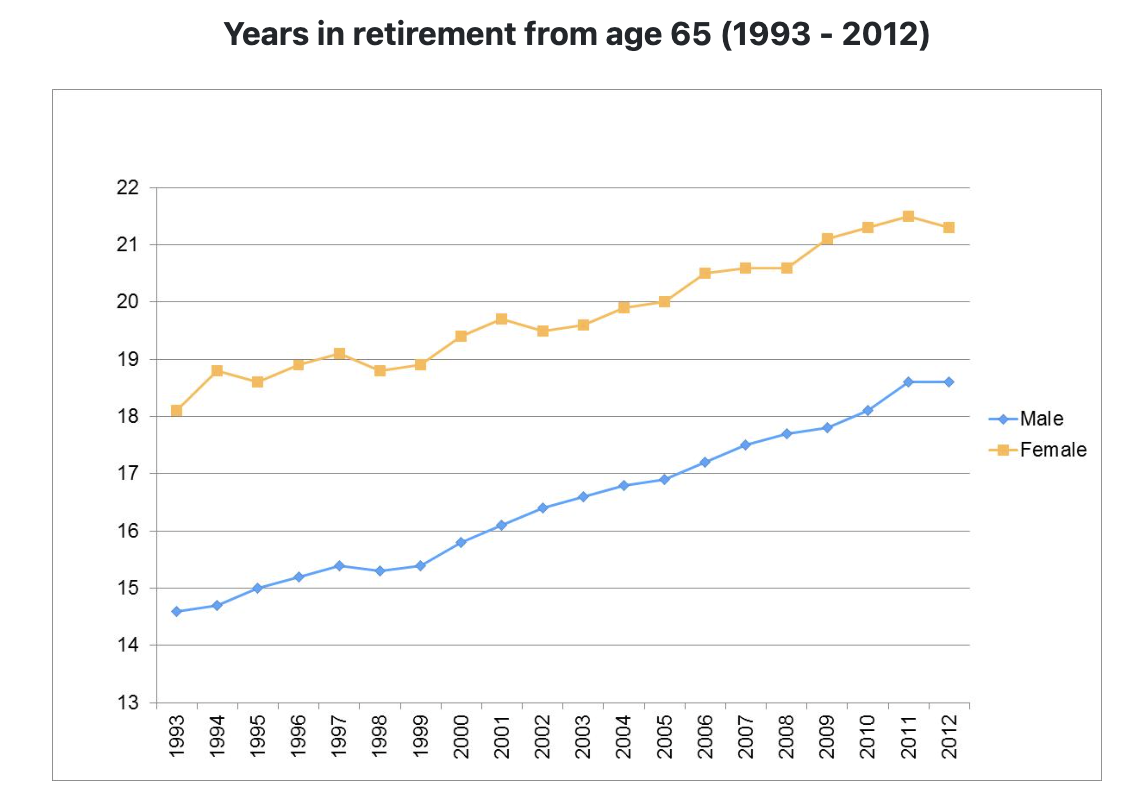

The chart below demonstrates the annual progression of the LGPS Life Expectancy Index between 1993 and 2012 for male and female E&W LGPS pensioners.

In this form the index clearly demonstrates how life expectancy in retirement has changed over time. It shows that life expectancy in retirement (measured from age 65) has increased from 14.6 years in 1993 to 18.6 years in 2012 for males and from 18.1 years in 1993 to 21.3 years in 2012 for females.

The average rate of increase in life expectancy has been around 2.2 years per decade for males and around 1.7 years per decade for females. Note that life expectancy does not increase steadily over the 19 year period, while in some years it increases rapidly, in other years it is unchanged or even falls.

Methodology

The LGPS Life Expectancy Index tracks the life expectancy of E&W LGPS pensioners. The methodology ensures the index results are objective and reflect the experience of E&W LGPS members.

The index is based on period life expectancy from age 65. For each year this is a measure of how long you expect to make pension payments to an average member based on death rates in that year.

This approach to measuring life expectancy uses only observable, verifiable data (with data on circa 2/3rds of E&W LGPS pensioners used by the index) and avoids any need for subjective assumptions about how life expectancies will change in the future.

The index allows changes in life expectancy from year to year, and trends in life expectancy emerging over a number of years, to be clearly identifiable.

Reliances and Limitations

- The life expectancy values shown in this chart have been provided by Club Vita to the Advisory Board for inclusion in the Scheme Annual Report. Whilst they can be reproduced, they should not be relied upon or used for any other purpose without the written permission of Club Vita LLP and Hymans Robertson LLP.

- Life expectancies are based on the experience of English and Welsh LGPS Funds that have provided data to Club Vita as at July 2014.

- The life expectancy shown for a particular year is the period life expectancy measured at age 65 – this is based on the exposure and deaths occurring during that year, so do not make any allowance for changes in longevity before or after that year.

- To be clear, the life expectancies shown have been calculated from the crude mortality rates of E&W LGPS pensioners.

- The life expectancy of an individual LGPS pensioner will depend on many factors, including age, gender, health, wealth, future changes in mortality, etc. and the figures shown here are not intended to represent or predict the life expectancy of any one individual member.

Definition of Period Expectation of Life

Source: Office for National Statistics, “Life expectancy at age 65 by local areas in the United Kingdom, 2004-06 and 2008-10”, 19 October 2011

“Period expectation of life at a given age for an area in a given time period is an estimate of the average number of years a person of that age would survive if he or she experienced the particular area’s age-specific mortality rates for that period throughout the rest of his or her life. The figures reflect mortality among those living in an area in each time period, rather than mortality among those born in each area.” “Period life expectancy at age 65 in 2000 is worked out using the mortality rate for age 65 in 2000, for age 66 in 2000, for age 67 in 2000, and so on.” “Period life expectancies are a useful measure of mortality rates actually experienced over a given period, and for past years, provide an objective means of comparison of the trends in mortality over time, between areas of a country and between countries. Official life tables in the UK and other countries which relate to past years are generally period life tables for these reasons.”

Information on calculating a longevity index

The starting point for the LGPS Life Expectancy Index is the collection of a complete and reliable record of longevity experience data for the LGPS. Club Vita currently hold up to date experience data for c. two-thirds of E&W LGPS pensioners. This is more than sufficient to produce an initial E&W LGPS Life Expectancy Index. Funds that are not currently providing data are invited to contact Club Vita if they wish their data to be represented in the LGPS Life Expectancy Index.

Once data has been collected, the calculation steps involved in producing the LGPS Life Expectancy Index are broadly as follows:

- For a reference period (eg calendar year 2011) and a reference population (eg E&W LPGS pensioners) where data has been collated, determine the observed (“crude”) death rate at each age (65, 66, 67, etc).

- The crude death rate at each age is simply the number of deaths at that age divided by the number of people being observed at that age. So it is an observable (objective) quantity, measuring the proportion of people that died at each age.

- The period life expectancy from 65 can be calculated directly from the crude death rates, and is the average length of time an individual aged 65 would live for, based on those observed death rates.

Was this page helpful?