Funding

In line with other UK pension funds, each LGPS fund undertakes a local actuarial valuation every three years. The last triennial valuation of the LGPS local assets and liabilities was at 31st March 2022 (see below) and the next one will be as at 31st March 2025. The results of the 2022 valuations are available on this website, with all fund annual reports as well as a scheme-level summary report published. There are also separate four-yearly scheme-level valuations that take place across public service pensions schemes including the LGPS, but these are separately conducted and reported and not considered here.

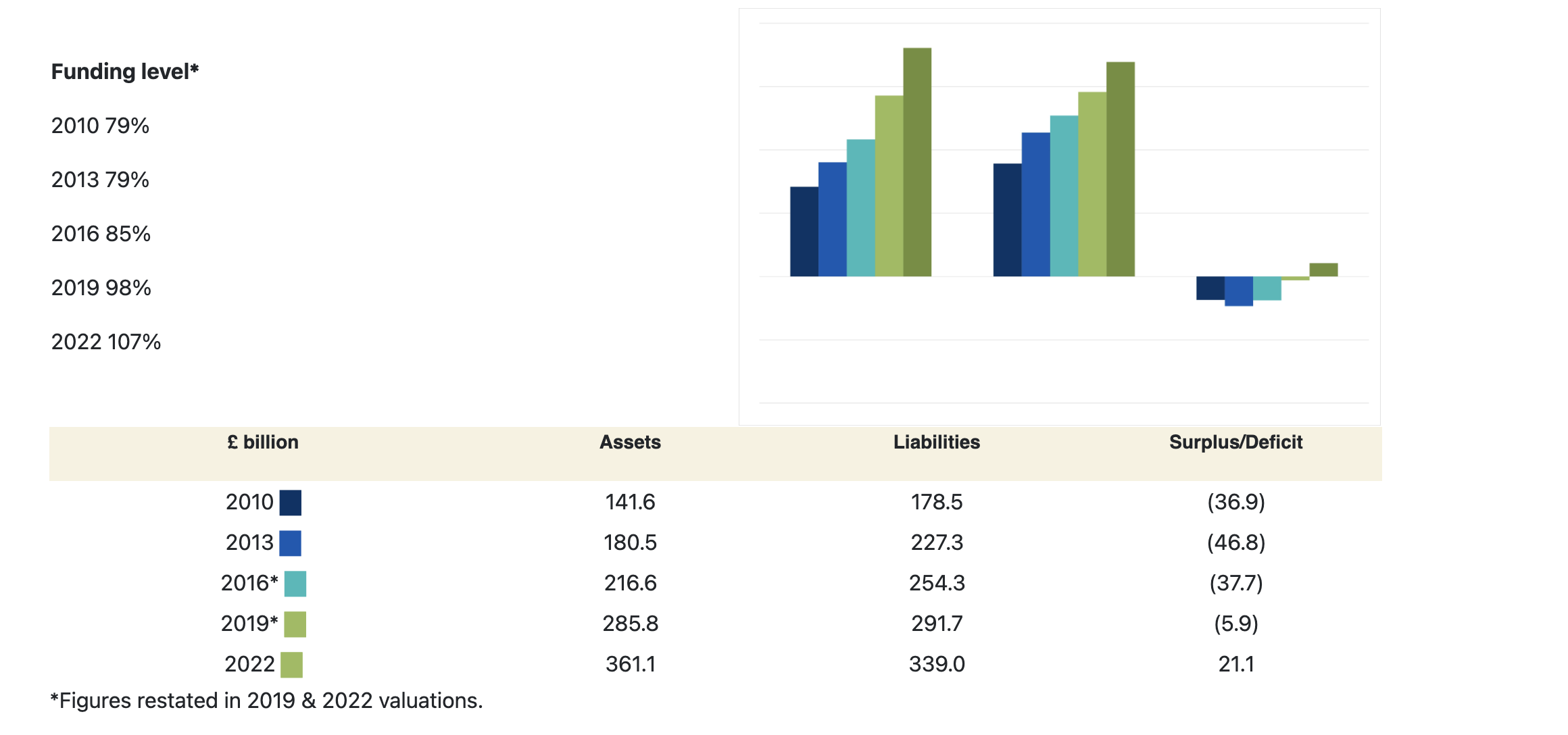

2022 Actuarial Valuation

The 2022 fund valuation results are available and are included here for reference. Together with Barnett Waddingham the Board has carried out an overall analysis of the 2022 valuations using LGPS fund data at 31st March 2022. Headline results and a comparison with 2019 is set out below. The 2022 valuation results were used to set employer contribution rates from 31st March 2023. It is important to note that each fund will have used different assumptions which makes direct comparisons across funds difficult. The overall analysis therefore is based on standardised information as set out in the valuation dashboard for each Fund (agreed between the Fund actuaries and the Government Actuary’s Department).

As at 31st March 2022, the analysis of the 2022 valuations reported assets of £361.1bn and liabilities on local funding assumptions of £339.0bn, i.e. a surplus of £22.1bn and a funding level of 107%. This is an overall improvement compared to the position in 2019 which showed assets of £285.8bn and liabilities of £291.7bn i.e. a deficit of £5.9bn and a funding level of 98%.

By way of comparison as at 31st March 2016, the funding level of the 5,131 direct benefit occupational pension schemes within the Pension Protection Fund index was 111.4% (on a insurance buyout basis, which is different from the LGPS actuarial valuation methodology). As at 31st March 2022 the University Superannuation Scheme funding level was 98%.

*See valuation 2013, 2016 and 2019 pages for fund values used in calculations.

2022 LGPS funding level £ billion

Development of LGPS funding position

Following the 2016 and 2019 valuations, the Board published two summary reports. A summary version outlined the key findings of the valuations and provided some brief background. A more detailed version gives a fuller overview of the 2019 valuations and provided some wider context as to a) how employer contribution rates are calculated during valuations, and b) how individual fund valuations relate to the Board cost management process. The Board has also published a detailed report on the 2022 valuation which highlights the improvement in funding position driven by asset performance, the increase in membership and decreased average total contribution rates.

Aggregated information

We have the following aggregated information from the annual report and audited accounts of the LGPS funds as of 31st March 2023 showing the development of the LGPS.

| 2023 | 2022 | 2021 | 2020 | 2019 | 2018 | 2017 | 2016 | 2015 | 2014 | |

|---|---|---|---|---|---|---|---|---|---|---|

| Number of actives (000) | 2,152 | 2,049 | 2,018 | 2,019 | 1,957 | 2,010 | 1,964 | 1,899 | 1,905 | 1,819 |

| Number of deferred (000) | 2,337 | 2,384 | 2,328 | 2,307 | 2,214 | 2,159 | 2,078 | 1,859 | 1,834 | 1,723 |

| Number of pensioners (000) | 2,005 | 1,955 | 1,881 | 1,833 | 1,728 | 1,691 | 1,642 | 1,530 | 1,512 | 1,459 |

| Total value of assets | £354bn | £369bn | £342bn | £276bn | £291bn | £275bn | £263bn | £217bn | £217bn | £192bn |

| Net return on Investment | -1.8% | 8.1% | 20.7% | -4.8% | 6.2% | 4.4% | 19.4% | 0.1% | 12.1% | 5.9% |

| Total contributions paid | £11.1bn | £11.6bn | £13.9bn | £10.2bn | £9.5bn | £11.8bn | £9.7bn | £9.3bn | £9.6bn | £8.7bn |

| Total benefits paid | £13.0bn | £12.6bn | £12.0bn | £11.1bn | £10.5bn | £9.9bn | £9.7bn | £9.4bn | £9.0bn | £8.6bn |

| Inflation (CPI) (change over previous 12 months to September) | 3.2% | 8.8% | 0.5% | 1.7% | 2.4% | 3.0% | 1.0% | 0.0% | 1.2% | 2.7% |

Income and Expenditure, year to 31st March 2023

| Cashflow in (£bns) | 2023 | 2022 | 2021 | 2020 | 2019 | 2018 | 2017 | 2016 | 2015 |

|---|---|---|---|---|---|---|---|---|---|

| Contributions & Transfers from Other Pension Funds | 12.1 | 11.58 | 13.87 | 11.74 | 10.67 | 11.79 | 10.91 | 9.82 | 12.66 |

| Net Investment income | 5 | 4.6 | 3.79 | 4.49 | 4.48 | 4.44 | 3.96 | 3.61 | 3.6 |

| Total income | 17.1 | 16.18 | 17.66 | 16.23 | 15.15 | 17.62 | 14.87 | 13.43 | 16.27 |

| Cashflow out(£bns) | 2023 | 2022 | 2021 | 2020 | 2019 | 2018 | 2017 | 2016 | 2015 |

|---|---|---|---|---|---|---|---|---|---|

| Benefits & Payments to Leavers | 13 | 12.58 | 12 | 12.12 | 11.51 | 10.38 | 10.33 | 9.92 | 12.29 |

| Administration expenses (including oversight and governance) | 0.27 | 0.23 | 0.22 | 0.22 | 0.2 | 0.18 | 0.19 | 0.18 | 0.11 |

| Investment management expenses | 1.74 | 1.87 | 1.49 | 1.3 | 1.16 | 1.04 | 0.88 | 0.81 | 0.73 |

| Total expenditure | 15.01 | 14.68 | 13.71 | 13.64 | 12.86 | 12.6 | 11.39 | 10.91 | 13.13 |

Cashflow before investment income

When looking at the gap between contribution income and benefit payments (i.e. excluding investment income), cashflow levels between funds ranged from -£382m to +£24m with the average being -£33.8m. 64 (75%) funds reported a negative cashflow on that basis. This compares to a range of cashflow positions between funds of -£410m to +£49m and an average of -£35m in 2022.

There are therefore an increasing number of funds looking to balance the need for asset growth to pay future benefits and using assets for income generation to pay benefits now. However, it is difficult to draw too many conclusions about the specific changes from year to year as these are strongly affected by the profiling of employer contributions across the valuation period.

Life expectancy index

Working closely with the LGPS Scheme Advisory Board, Club Vita have created an LGPS Life Expectancy Index to communicate the evolution of life expectancy amongst LGPS pensioners in a simple and informative way. The Index also provides the Board an early warning signal of material changes in longevity that might impact the affordability of benefits.

In addition to the LGPS Life Expectancy Index, Club Vita provides valuable longevity analytics to the majority of UK LGPS funds. This enables funds and their advisers to understand the evolution of fund specific longevity. It also means that the longevity assumptions, used to value liabilities at the triennial valuation, can be selected to reflect the specific demographic profile of the fund’s membership. Funds which don’t currently receive Club Vita longevity analytics are invited to contact Jill Jamieson, Head of Pensions UK at Club Vita.

This year’s Life Expectancy Index focuses on the latest available mortality data for LGPS pensioners up to the end of 2022. It is presented as single data points for men and women considering only death rates in the particular year.

The Index shows the drop in life expectancy at age 65 in 2020, back to levels last observed in 2010. Despite losing a decade of longevity improvements during the worst of the pandemic, the Index illustrates that life expectancies bounced back over 2021 and continued to improve in 2022. Whilst our estimates are based on emerging data, the latest point on the Index suggests that average life expectancies observed in 2022 were slightly higher than 2019. This is perhaps the first indication that LGPS pensioner life expectancy may be returning to pre-pandemic trend, with mortality improvements at the modest levels observed during the 2010s.

Given the diverse membership and long-term focus of the LGPS, it is important to consider wider longevity trends and the impact they could have on the future life expectancy of different types of individuals participating in the LGPS. For example, funds receiving Club Vita’s services have access to longevity analysis that takes account of specific regional and socio-economic factors at the individual member level.

For the latest analysis on post pandemic longevity trends, please visit the Club Vita website.

Changes in observed longevity

The chart below demonstrates the annual progression of the LGPS Life Expectancy Index between 1993 and 2022 for female and male LGPS pensioners in England and Wales (E&W). It measures the years that members are expected to live in retirement for, after reaching the age of 65, based on death rates in that year (referred to as period life expectancy).

Recent mortality experience observed in the general population

Deaths amongst the UK population rose rapidly over April and May 2020 as the pandemic arrived and before lockdowns began to limit the spread of the virus. Following a resurgence in CoViD-19 deaths in the last few months of 2020, the death count for the year was around 83,000 higher than is expected. Given a typical year sees UK deaths of around 600,000, the 83,000 figure illustrates the impact of the pandemic, despite the significant social distancing measures put in place.

The Delta and Omicron variants spread throughout 2021 and CoViD-19 deaths replaced the usual winter “mortality spike”. By the end of 2021, the death count for the year was around 60,000 higher amongst the general population than is typical.

2022 was another year of heavier mortality within the UK population. Whilst milder than 2020 and 2021, we again saw more deaths in the UK than expected under pre-pandemic projections, with these ‘excess deaths’ observed in the summer months and through to the end of the year.

As discussed in a recent blog, fully understanding 2023 mortality experience requires careful analysis. December 2022 was a period where we observed unusually late reporting of deaths and, in late 2023, the ONS published revised population estimates following the 2021 census. Both the time at which deaths are reported and the level of the living population are key components of calculating mortality rates. If we make some optimistic assumptions to adjust the previously reported figures for these considerations, we may be beginning to see signs that life expectancies in the general population are beginning to reach pre-pandemic levels. We should note that this is only a single data point and the figures continue to rely on estimates. However, further analysis on 2023 life expectancies, including specific insights on LGPS pensioner longevity will be available in our next index.

Recent mortality experience observed amongst LGPS pensioners

In general, LGPS pensioners have been somewhat insulated from some of the population health effects we have observed in recent years. Whilst we observed decreases in period life expectancy in 2020 at both the national level and the LGPS pensioner level, local pockets of COVID-19 infections and deaths led to regional variations in mortality rates, which could be linked to socio-economic variation.

Similarly, analysis from the LGPS Life Expectancy Index in 2021 and 2022 suggests that pensioners are seeing a more pronounced bounce back towards pre-pandemic life expectancies than the general population. Again, this could be linked to socio-economic factors within the LGPS membership alongside the financial buffer that comes with receiving a guaranteed retirement income from an LGPS fund.

This phenomenon is not unique to the time since CoViD-19. Longevity trends in general (in particular since 2011) have not affected DB pensioners in the same way as the general population and indeed have affected different DB pensioners to differing extents, depending on an individual’s socio-economic status.

As such, it’s important for LGPS funds to understand the socio-economic profile and regional concentration of their fund and understand what this could mean for life expectancies – using population statistics for assumption setting, and risk management, could be potentially misleading. No two LGPS funds will be impacted to the same extent and in fact, no two employers within a fund will see the same mortality impacts in relation to evolving longevity trends.

Club Vita continues to monitor the differing longevity trends of different socio-economic groups across the “Comfortable”, “Making-Do” and “Hard-Pressed” sub-groups of the Club Vita dataset. Essentially, these groups divide the Club Vita DB pensioner data into high, medium and low socio-economic groups which we refer to as VitaSegments. VitaSegments then enables LGPS funds and their actuaries to set longevity trend assumptions that reflect the bespoke socio-economic characteristics of the membership, rather than relying on E&W population figures which may not truly reflect the members’ circumstances.

Applying the E&W population trend to a group of pensioners could see future life expectancy underestimated for more affluent pensioners. Underestimating the life expectancy (and therefore the associated liabilities) of higher socio-economic groups is most problematic, as we generally see the majority of a fund’s liability concentrated on these higher socio-economic groups.

Consequences for LGPS Funds

What should LGPS funds (and their actuaries) do about this as they consider the risks facing the fund in the run up to their next valuations? They will typically take a longer-term view, seeking to base their funding assumptions for longevity on a broader view of how longevity has been changing rather than reacting to the most recent experience alone.

Given the volatile experience to date and the early evidence on how different individuals are being impacted by the aftermath of the pandemic, understanding the socio-economic profile and regional concentration of the fund membership becomes important, together with a view on whether different drivers of mortality improvements will affect different groups in different ways. These will inform both the current rate of longevity improvement amongst fund members and views on how that will change over the next 2 or 3 decades. These long-term drivers of longevity have the potential to generate a much more material impact on liabilities than what we have seen over the last few years as a result of the pandemic.

Once appropriate longevity assumptions have been set, taking account of the specific socio-economic profile and regional concentration of the fund membership, some LGPS funds (and their actuaries) use scenario analysis to stress test their longer term funding strategy. A good example of a phenomenon with the potential to significantly disrupt life expectancy is climate change. Club Vita have prepared a paper on how climate change and resource constraints might impact UK longevity. This introduces three climate change longevity scenarios which some LGPS funds have used to explore the effects of climate change on their funding plans.

Impact on life expectancy is shown for a 50-year-old based upon life expectancy upon reaching age 65 and is average across men and women. Calculations are relative to prevailing typical UK projection used by pension schemes at the time of publication of these scenarios (2018). Impact shown for a typical scheme and are intended to be indicative only. For more information see Club Vita | UK | Hot and Bothered?

Club Vita are regularly refreshing a suite of scenarios on a wide range of drivers such as healthcare and lifestyle disruption. These scenarios, together with considerations of other risks such as investment risk, can help pension funds introduce longer term longevity considerations into their risk management framework.

Methodology

The LGPS Life Expectancy Index tracks the life expectancy of E&W LGPS pensioners. The methodology ensures the Index results are objective and reflect the experience of E&W LGPS members.

The Index is based on period life expectancy from age 65. For each year this is a measure of how long you expect to make pension payments to an average member based on death rates in that year.

This approach to measuring life expectancy uses only observable, verifiable data (with data on circa 2/3rds of E&W LGPS funds used by the Index) and avoids any need for subjective assumptions about how life expectancies will change in the future.

The Index allows changes in life expectancy from year to year, and trends in life expectancy emerging over a number of years, to be clearly identifiable.

Reliances and Limitations

- The life expectancy values shown in this chart have been provided by Club Vita to the Advisory Board for inclusion in the Scheme Annual Report. Whilst they can be reproduced, they should not be relied upon or used for any other purpose without the written permission of Club Vita (UK) LLP.

- Life expectancies are based on the experience of English and Welsh LGPS funds that have provided data to Club Vita as at February 2024.

- The life expectancy shown for a particular year is the period life expectancy measured at age 65 – this is based on the exposure and deaths occurring during that year, so does not make any allowance for changes in longevity before or after that year.

- To be clear, the life expectancies shown have been calculated from the crude mortality rates of E&W LGPS pensioners.

- The life expectancy of an individual LGPS pensioner will depend on many factors, including age, gender, health, wealth, future changes in mortality, etc. and the figures shown here are not intended to represent or predict the life expectancy of any one individual member.

This report does not constitute actuarial advice but rather a set of information to support the Advisory Board in communicating the evolution of life expectancy amongst LGPS pensioners.

This report has been prepared in line with the principles of the Financial Reporting Council’s Technical Actuarial Standard (TAS) 100: Principles for Technical Actuarial Work.

Appendix 1 Definition of ‘Period expectation of life’

Source: Office for National Statistics, “Life expectancy at age 65 by local areas in the United Kingdom, 2004-06 and 2008-10”, 19 October 2011

“Period expectation of life at a given age for an area in a given time period is an estimate of the average number of years a person of that age would survive if he or she experienced the particular area’s age-specific mortality rates for that period throughout the rest of his or her life. The figures reflect mortality among those living in an area in each time period, rather than mortality among those born in each area.” “Period life expectancy at age 65 in 2000 is worked out using the mortality rate for age 65 in 2000, for age 66 in 2000, for age 67 in 2000, and so on.” “Period life expectancies are a useful measure of mortality rates actually experienced over a given period, and for past years, provide an objective means of comparison of the trends in mortality over time, between areas of a country and between countries. Official life tables in the UK and other countries which relate to past years are generally period life tables for these reasons.”

Appendix 2 Calculation of period life expectancy Information on calculating a longevity index

Information on calculating a longevity index

The starting point for the LGPS Life Expectancy Index is the collection of a complete and reliable record of longevity experience data for the LGPS. Club Vita currently hold up to date experience data for c.2/3rds of E&W LGPS Funds.

Once data has been collected, the calculation steps involved in producing the LGPS Life Expectancy Index are broadly as follows:

- For a reference period (e.g. calendar year 2011) and a reference population (e.g. E&W LPGS pensioners) where data has been collated, determine the observed (“crude”) death rate at each age (65, 66, 67, etc).

- The crude death rate at each age is simply the number of deaths at that age divided by the number of people being observed at that age. So it is an observable (objective) quantity, measuring the proportion of people that died at each age.

- The period life expectancy from 65 can be calculated directly from the crude death rates and is the average length of time an individual aged 65 would live for, based on those observed death rates.

Report pages

Was this page helpful?